In a context marked by decarbonization and the accelerated growth of renewable energies, electrical systems face a new challenge: it is no longer enough to manage generation, it is also necessary to manage consumption.

Although not a recent concept, demand flexibility has gained momentum in the last 15–20 years and today it is emerging as a key strategic asset for the transition to decarbonized and more efficient electrical systems.

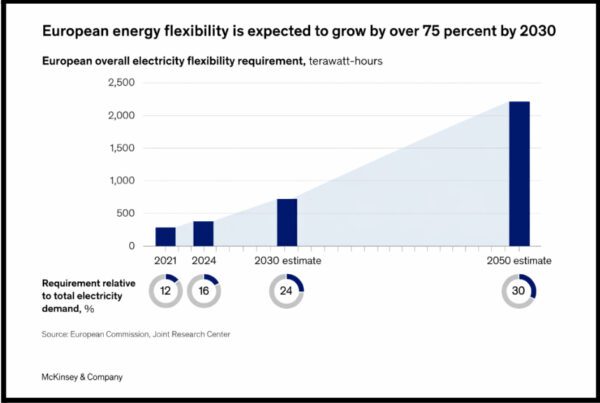

In fact, according to an article published by McKinsey in 2025, it is estimated that Europe could need 75% more flexibility by 2030, which opens the door to significant opportunities in the region.

The question here is not whether companies will participate in this process, but the opportunity cost they will leave on the table if they do not.

Why do we talk about a strategic asset?

Demand flexibility is the ability of consumers to modulate their electricity consumption in response to market signals or technical conditions of the grid, avoiding the activation of less efficient and more expensive additional generation units.

This modulation can involve reducing, delaying or even increasing consumption at specific moments, aligning it with renewable availability or with more favorable market prices.

In any case, if the consumer has the necessary tools and proposes a clear strategy, they will find in flexible demand a potential source of income and improvement of competitiveness.

Business paradigm shift

Capturing this added value implies a paradigm shift within companies: energy must stop being managed as a fixed cost, it must be managed as a strategic asset capable of generating income and strengthening the resilience of processes.

Participating in flexibility markets implies:

- INVESTMENT in digital tools, control and monitoring systems.

- STUDY and OPTIMIZATION of processes.

- REGULATORY IMPLICATIONS.

- RESTRUCTURING and COORDINATION of the different departments.

- DESIGN of a strategy and control of objectives.

It is not an easy path, but it is clear that those who get ahead and are able to adapt and transform the way they manage their energy will obtain a greater competitive advantage in this new scenario.

Markets where flexibility materializes

Flexibility becomes value through specific electricity markets that can be grouped into three main categories:

1. Balancing markets: real-time stability

Managed by the system operator, they seek to maintain an instantaneous balance between supply and demand and thus guarantee a constant frequency.

To participate in these markets it is necessary to have technical authorization (telemetry, rapid response capacity, minimum available power) and the client is remunerated for providing a technical service to the system.

2. Energy markets: economic optimization

They go beyond the technical part and seek economic optimization in the bill.

- Daily market (Day-ahead), which, in the case of the Iberian Peninsula, is operated by OMIE.

- Intraday market (Intra-day), which allows positions to be adjusted after the closing of the daily market.

In these markets the client participates as a market agent or through a representative. Participation is reduced to an adjustment of forecasts and shifts in consumption towards more economical hours or outside of peak price hours. The remuneration here is indirect, since it does not exist as such, but the impact is seen directly on the final bill.

3. Capacity and congestion mechanisms: structural security

These markets seek to remunerate future availability or the management of localized restrictions.

- Capacity markets, where the system operator pays for availability to reduce consumption at critical moments.

- Congestion management services, where localized flexibility is sought to avoid overloads in certain areas of the grid.

Here the client is remunerated for providing services that reinforce the structural resilience of the grid and energy security.

Demand response as an attractive option

Demand response is presented to companies as a particularly attractive option. It is an affordable and reliable solution that can be integrated directly into production and consumption decisions. In addition, it combines several advantages:

- Protection against price volatility: reduces exposure to market peaks.

- Rapid scalability: can be implemented with minimal operational disruption.

- Low capital requirement: does not require large infrastructures such as batteries.

- Tangible economic impact: currently represents +/-10% of the flexibility supply in some countries, and is expected to double by 2030.

In Spain, this service is provided through the SRAD (Active Demand Response Service) and is today the clearest and most direct instrument for participation in demand for companies.

SRAD in Spain

The SRAD is managed in Spain by Red Eléctrica and allows it, in its role as system operator, to request a temporary and programmed reduction of their energy demand from large consumers, in exchange for financial compensation.

In 2025, for example, the companies participating in this mechanism could receive up to €246,000 annually in remuneration for each 1 MW of committed power.

Companies participate through a competitive auction mechanism in which participants submit their offers and REE selects those that are most efficient for the system.

In this process, the participants agree to reduce a certain amount of their electricity consumption (active power) when REE requests it. The activation of the service must be fast, with a response time of less than or equal to 15 minutes from when activation is required and for a maximum of three hours.

The assigned beneficiaries receive remuneration for the availability of reducing their demand (a fixed sum for availability) and an additional amount for each opportunity in which the activation of the service is required.

This year, REE will have a total of 1,725 MW of power to provide greater flexibility to the operation through the SRAD. This volume means an increase of 50% compared to the power available in 2025.

Challenges and barriers for the future

It is clear where we are going in terms of energy management strategies. However, the road is not without challenges. The lack of a clear regulatory framework and stable price signals in the markets are one of the main challenges for the future. In addition, the need for investments in automation and control technologies and the integration of the participating actors in the market, remain an unknown in this process, which sooner or later must be resolved.

The recent approval of the general regulation of supply, commercialization and aggregation of electrical energy in Spain last Tuesday represents a great advance in regulatory matters. In this package of announcements, the legal definition of the role of independent aggregator stands out, where its rights, obligations and operational requirements are established, in very similar terms to the commercializers.

These figures will be able to group consumption or energy generated by consumers, producers or storage systems to buy or sell in the electricity markets, especially in the balancing markets, offering active demand management services. For its part, the consumer will have the possibilit of freely contracting an aggregator to optimize their electricity demand, and may obtain savings on their bill, without this affecting their supply contract with the commercializer.

This recent news makes one thing clear to us: The energy transition towards decarbonized systems will not be achieved solely by building more capacity and renewable infrastructure. The real structural change will occur when the system evolves, ceases to be unidirectional and makes the consumer a relevant actor in the process.

Matías Curletto I Energy Expert

If you found it interesting, please share it!

Recent Articles