In 2006, Al Gore’s documentary entitled “An Inconvenient Truth” shocked the World with a catastrophic scenario that we would be facing if drastic measures wouldn’t be taken. Expressions like global warming, climate change, sustainable growth, air pollution, green energy, etc. gained momentum and energy, environmental and economy policy roadmaps were developed and implemented to avoid that scenario. However, coal demand kept rising until 2014. According to the recent BP Statistical Review of World Energy 2016, published on 20th June (latest version), coal consumption fell about 1.8% in 2015, corresponding to an amount of 71 Mtoe, a drop never registered in 50 years of BP’s statistics.

Illustration 1 – World coal consumption until 2015. Source: BP Statistical Review of World Energy 2016 – Magnus CMD

Of course coal had, in its long history, some setbacks normally following recession years like the Asian financial crisis in 1997 and the global financial crisis in 2008, but for 2015(click here to see all the coal trades in 2015), the global economy actually grew 3% and yet coal prices were far from healthy. So what happened to cause this historical drop?

Coal Trade around the world – BP

Giant China Slowing Down

Global extraction of all primary coal kinds passed from 3 Gigatonnes (Gt) in 1972 to 4 Gt in 1983. After the beginning of the new millennium, the growth rate was around 1 Gt per 3 years as consequence of the production intensification in China. Production increased at a rate of 176.8% against the 78.4% of the rest of the world.

In 2015, the Republic of China consumed half of all the coal extracted that year, from which, only 7% were imported and the remain was domestic. As expected, the slow signals received in 2014 for a slowing down Chinese economy resulted in a fall of 1.5% in coal consumption, i.e. from the 1920 Mtoe consumed by China in 2015, 291 Mtoe were imported, majorly from Australia.

Illustration 2 – China coal imports 2000-2015. Source: UN Comrade Database – Carbon Brief

U.S.A. Energy Shift

The success of U.S. shale gas and the struggle against climate change were the main tools for the change that we are witnessing in Uncle Sam’s national energy mix. The biggest victim of this change is coal that have been losing margin year on year, registering a fall of 13% from 2014 to 2015.

However, coal is still the first source of energy in the U.S. contributing with more than 30% of the national energy mix, followed (closely) by Natural gas and with nuclear standing at a solid third position. In spite of huge efforts and investments done in the past years, renewables contribute with less the 10% of the energy mix.

Another concern regarding the future of U.S. coal is exports. With the rapid energy technology shift in 2010, major American producers turned their efforts to outside the boarders, increasing their exports from 87 Mtoe to 131 Mtoe in just two years. Nonetheless, the slowdown of the global economy, especially in China, along with the low carbon goals established in EU has been affecting global coal exports and US was not immune to that. In fact, the decline of domestic consumption and the reduction of coal exports by 44% from the 131 Mtoe from 2012 to 2015, made America’s biggest coal miner, Peabody Energy, to file for bankruptcy in April this year, following eight more similar companies that did the same in the previous year.

Illustration 4 – US Coal Exports 2000-2015. Source: UN Comtrade Database – Carbon Brief

Asia As The Main Target!

The COP 21 held last year in Paris marked a blurred future for coal sector, were 200 countries agreed to take strict measures and goals to fight global warming. Being the biggest energy source of air pollution, this raw material is being ruled out from all developed countries. In the other hand, developing countries seem to be serving as a buffer to prevent a steeper fall in coal market.

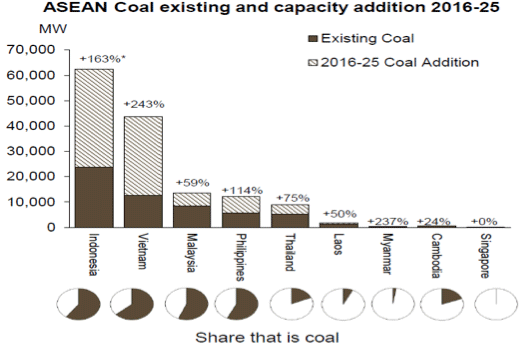

Even with the current slowdown of China, all the Asian emerging economies (China included) intend to increase their coal output capacity and consumption until 2030. At the 22nd Coaltrans Meeting, the coal sector got optimistic as the long-term projected coal capacity additions in India, China and Southeast Nations demonstrated great forecasts of growth. According to the data showed in May at this Meeting, held in Bali, more than 530 GW will be installed in those nations between 2016 and 2025.

Is important to mention that from this 530 GW new capacity, 345 is allocated to China, so this number can be shorter than expected.

Illustration 5 – ASEAN coal capacity addition by 2025. Source 22nd Coaltrans Meeting

Europe: Coal vs Nuclear

The 2020 goals defined by all European union members and reinforced with the recent Paris COP21, result in more bad news for coal industry. According to the most recent Polices Scenarios, coal demand will drop by 65% by 2040, which represents more than 300 Mtoe, being replaced mainly by renewables and some natural gas in the energy mix.

However, it is possible to verify different approaches to reach the EU targets chose by some members.

Taking UK for example, The Report “KEEPING THE LIGHTS ON: Security of supply after coal” developed by Bright Blue, presents a study where different scenarios are defined to accomplish a total phase out of coal by 2025. If accomplished, UK, the first to use coal do produce electricity, will be the first country in the world to keep energy security without using it.

Germany, on the other hand, instead of a phase out of coal, intends to shut down all the nuclear power plants by 2022, something they planned to do since the episode of Fukushima back in 2011. In spite of the environmental goals defined where Germany has to reduce its greenhouse gas emissions by 80 to 95% of 1990 levels by 2050, in 2015 coal contributed for 44% of the energy mix, where 11% of that mix was from other fossil fuels (oil and natural gas). According to the Energy Road-map for 2050, renewable energy is expected to grow between 40 to 45% until 2025 and more than 80% by 2050 (compared with current levels). If the German priority is to eradicate nuclear power, is expected that until 2025, coal will contribute with more than 40% of the energy mix making the environmental targets much more difficult impossible to be achieved.

Be Aware With India

India is in position of dethroning China as the world’s biggest coal importer as the demand for energy, around the country, increases exponentially. However, Indian Energy Minister, Piyush Goyal affirmed in April, that India wants to stop importing coal by finding new reserves and by increasing the power capacity through coal. Since China’s current strategy already affects its top exports that are also the major sources of India’s imports, a scenario where China and India reduce largely their levels of imports, Australia, Indonesia and South Africa could face a complicated situation.

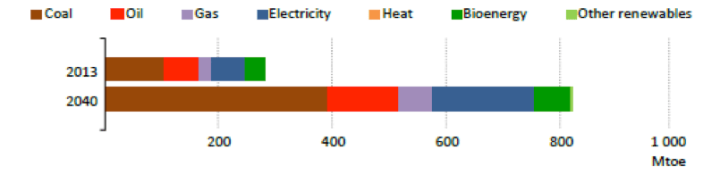

IEA latest reports show that, in 2012, 72% of total electricity consumption in the country comes from coal-fired plants which mean a consumption of 360 Mtoe. The same entity claims that installed capacity will double by 2040, which is not good news for the environment since India already has 11 of the 20 most pollutant cities in the world. Nevertheless, the Climate Program defined really strict and specific rules for the coal sector in terms of technology and emissions control.

Illustration 6 – Indian Energy Mix evolution until 2040. Source: IEA – Energy and Air Pollution

Besides all the development expected in Asia for the next years, India is already the third largest emitter of GHE gases so if measures are not taken and supervision doesn’t take place, the COP21 efforts made by 200 nations can be insufficient to prevent reaching the 2.0 Celsius degree of global temperature.

Coal, the most abundant energy source in the globe but also the most pollutant seems to have a future, it may be less bright than before, but its end is far away. This commodity still will be a major participant in the energy mix and in the industrial sector, so the biggest question will be how effective and efficient will be the new coal technologies and how strict will be policies defined for this commodity to prevent the increase of GHE and air pollution.

Jorge Seabra | Energy Consultant

If you found it interesting, please share it!

Recent Articles