Introduction and European Sustainability Goals

In a world facing unprecedented environmental and energy challenges, the European Union is positioning itself as a key player in sustainability and energy transition. The sustainability goals set by the EU have been hailed as ambitious milestones for the future of our planet. However, the question is whether these goals are achievable or whether they remain a distant utopia.

The European sustainability goals, as set out in the European Green Deal and the Fit for 55 package, aim to radically transform the way we produce and consume energy, while reducing our greenhouse gas emissions. Key targets include reducing CO2 emissions by 55% by 2030 compared to 1990 levels, as well as the ambitious goal of achieving carbon neutrality by 2050.

These goals are not simply distant aspirations; They are essential to respond to the climate emergency and ensure a sustainable future for future generations. However, achieving them faces a range of complex challenges, ranging from physical limitations to the political and economic obstacles of the energy transition.

Realism of objectives:

Let’s take a closer look at the reality of European sustainability goals. While progress has been made in some regions, it is clear that the EU is still far from achieving its ambitious targets. CO2 emissions continue to fall, but at a rate insufficient to meet the 2030 targets. According to Member States’ latest projections, the net reduction in emissions would only be around 41% by 2030, far from the 55% initially planned. To meet the 2030 emissions reduction target, the pace of annual greenhouse gas emission reductions in Europe needs to more than double the annual progress made since 2005.

Key challenges include divergent national policies, conflicting economic interests and industry pressures. The coal industry, for example, continues to exert considerable influence in some EU countries, delaying the transition to cleaner energy sources such as in Germany (24% of electricity produced with coal), with the abandonment of nuclear power and geopolitical tensions with Russia. A policy opposite to that of the development of nuclear power in France or even more recently in the United Kingdom. In the context of the relocation of European industries after covid, the question arises about their ability to remain competitive in the face of competition from emerging countries and the multiplication of mechanisms for decarbonization. The latest forecasts have revised the expected growth downwards for 2024, with a growth rate that is not expected to exceed 0.8% for the European Union. This slower-than-expected pace is in line with an overall slowdown in the European economy. In this economic context and with the economic austerity measures adopted in many Member States, are the decarbonisation targets really realistic?

The physical limits of the energy transition:

The energy transition towards cleaner and more sustainable energy sources faces several physical limitations that can hinder its effective implementation. Among these limitations, the increasing and sometimes exponential demand for material resources is at the forefront. Essential for the manufacture of green technologies such as solar panels, wind turbines and batteries, these materials are essential for the transition to a low-carbon economy.

At the center of these concerns are lithium and cobalt. Although poorly represented in the table, unlike copper and aluminum, they are used in batteries and electric vehicles, which alone account for more than half of the growth in mineral demand over the next two decades and are considered materials whose production is at a critical point. Depending on the technology chosen, demand varies enormously in the different scenarios proposed: demand for lithium in 2040 could be 13 times higher (if vanadium redox flow batteries enter the market quickly under the STEPS* program) or 51 times higher (if solid-state batteries are brought to market faster than expected under the SDS* program) than current levels. Cobalt could be in demand 6 to 30 times higher than it is today, depending on how battery chemistry evolves.

In addition, the extraction of these resources can lead to significant environmental and social consequences. Mining sites can lead to the degradation of local ecosystems, soil and water pollution, as well as conflicts with local communities.

Finally, the depletion of natural resources is a major concern. Deposits of rare metals are not inexhaustible, and their intensive exploitation can quickly deplete available reserves. Indeed, according to some sources, a deficit of up to half of the need for lithium and cobalt is forecast for 2030. This raises questions about the long-term sustainability of the energy transition and the need to develop recycling and recovery technologies to extend the life of existing resources.

Dependence on other regions

The European Union relies heavily on energy imports to meet its energy needs, making it vulnerable to price fluctuations on global markets and geopolitical tensions. The impact of geopolitical tensions such as we have seen between Russia-Ukraine and Israel-Hamas shows how energy sovereignty is a key response to a resilient energy system. Although these two conflicts have been assimilated by the markets, the next challenge lies in diversifying sources of supply and better preparing for possible problems in the supply chains of materials crucial to the energy transition.

*STEPS: Stated Policies Scenario

*SDS: Sustainable Development Scenario

This increased dependence exposes Europe to a number of risks, including price instability: +738% lithium, +156% cobalt, +94% nickel on the respective prices between 2021 and 2022; supply

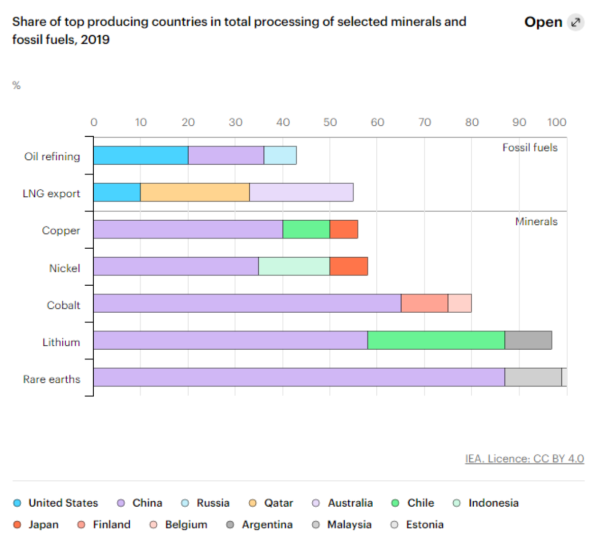

disruptions: Europe is more than 75% dependent on imports of key materials for the energy transition; and geopolitical tensions with major material suppliers: As we can see from the chart above, China accounts for more than 87% of the production of rare metals and a large majority of the production of minerals needed for the energy transition. In addition, the growing competition for access to these resources can intensify geopolitical rivalries and tensions between EU Member States and other regions of the world: the current situation in the DRC (Democratic Republic of Congo) where the various major world powers are scrambling for cobalt mining resources, or the US embargo on the production of materials from the Xinjiang region in China.

To reduce this dependency and strengthen Europe’s energy security, investments in interconnection infrastructure to facilitate cross-border energy trade and strengthening energy cooperation with neighbouring countries and international partners is crucial. In the SDS, the annual rate of network expansion is expected to more than double by 2040. About 50% of the increase in transmission lines and 35% of the increase in distribution grid lines are attributable to the increase in renewable energy. Effective recycling policies can also reduce the need for primary supply and play a key role in building a more sustainable energy landscape.

If you found it interesting, please share it!

Recent Articles