Few terms have become as common during the first half of the 2020s as energy transition, decarbonization, and net zero by 2050, all conveying that grand global goal of eliminating fossil fuel combustion, and the attendant emissions of CO2, by the middle of the 21st century –- and hence preventing further undesirable increases of tropospheric temperature. Genesis of this goal goes to the Paris Agreement of 2015 (COP 21) which stated that the world must “achieve a balance between anthropogenic emissions by sources and removals by sinks of greenhouse gases in the second half of this century”. The now common term “net zero” and the year of 2050 were used for the first time in the IPCC’s Special Report on a Global Warming of 1.5 ˚C in 2018: in order to limit the warming to 1.5 ˚C, global net anthropogenic CO2 emissions must “decline by about 45% from 2010 levels by 2030 . . . reaching net zero around 2050.” The Net Zero concept has been then grounded into a concrete road map by the IEA in a specific publication, “Net Zero by 2050 – A Roadmap for the Global Energy Sector” in May 2021, where the main pillars of the global decarbonization process have been set:

- Energy efficiency

- Behavioral changes

- Electrification

- Renewable energy (mainly solar PV and wind turbines)

- Hydrogen (i.e., Power-to-X)

- Bioenergy

- Carbon Capture and Storage (CCS)

The European Union set its energy and climate agenda accordingly: in December 2019, EU leaders meeting within the European Council agreed that the EU should achieve climate neutrality by 2050. Climate neutrality means to only emit as much greenhouse gas into the atmosphere as can be absorbed by nature, that is forests, oceans and soil. To reach such a net-zero emissions balance by 2050, EU countries will have to drastically reduce their greenhouse gas emissions and find ways of compensating for the remaining and unavoidable emissions. In its conclusions, the European Council underlined that the transition to climate neutrality brings significant opportunities for:

- economic growth

- markets and jobs

- technological development

EU leaders asked the European Commission to take forward work on the European Green Deal. They also recognized the need to ensure that the green transition is cost-effective, as well as socially balanced and fair. Exactly a year later, in December 2020, EU leaders took a further step towards climate neutrality. As an intermediate step towards the 2050 goal, they agreed to more than halve (compared to 1990 levels) the EU’s greenhouse gas emissions by 2030.

by 2030. This goal is a major step up from the EU’s previous 2030 target – agreed in 2014 – of cutting emissions by 40%.

Leaders called on the European Commission to put forward proposals so that countries can reach the 2030 goal, including by:

- improving green finance standards

- strengthening the EU’s emissions trading system

- spurring climate-friendly innovation

- ensuring fairness and cost-effectiveness

This call led to the ‘Fit for 55’ package. A set of proposals for revision of existing legislation and new initiatives, ‘Fit for 55’ is the EU’s key plan for turning climate goals into EU law. The package includes rules on:

- energy

- transport

- emissions trading and reductions

- land use and forestry

In continuous attempt to raise its goals and expectations and at a distance of only 2 years, very recently (last February), the European Commission defined another, very ambitious, intermediate goal on the road to “net zero by 2050”: 90% emissions reduction by 2040. This new 2040 target aims to enhance resilience against future crises and strengthen energy independence by reducing imports of fossil fuels.

However, beyond the big plans and political claims, how well is the proposed Net Zero road map of the European Commission grounded in current scientific, technical and economic consensus about the viability and timeline of energy transitions? What are the biophysical and economic realities that may hinder the EU commission plans? Let’s put some numbers in perspective.

Comparative scenarios of decarbonization up to 2045

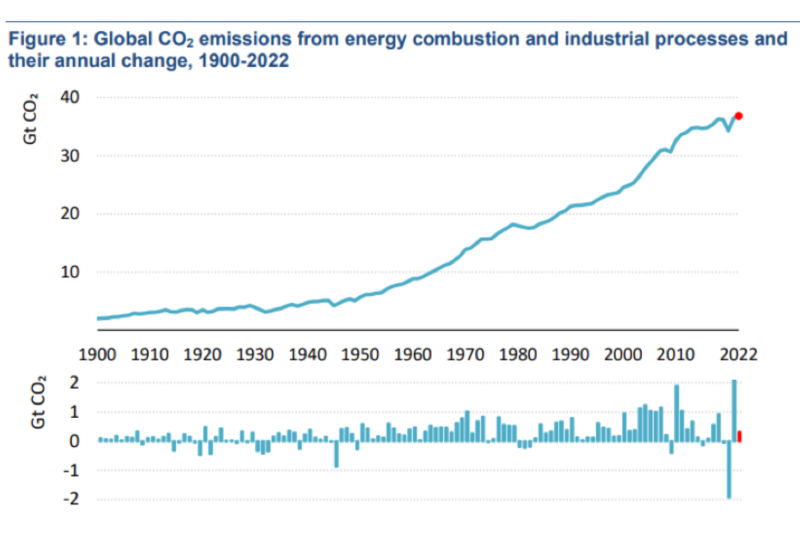

Whatever we are doing at the European level, climate change is inevitably a global issue, and despite the trillions already spent in green investments during the last 20 years, there is no evidence the global economy has tools to curb emissions other than economic crises (figure 1). Emissions are always on the rise except, recently, in the year 2008 and 2020. The historical series ends in 2022, but you can bet that in 2023 global CO2 emissions reached another record high, indeed at 37.4 billion tons, a 1.1% increase compared to 2022.

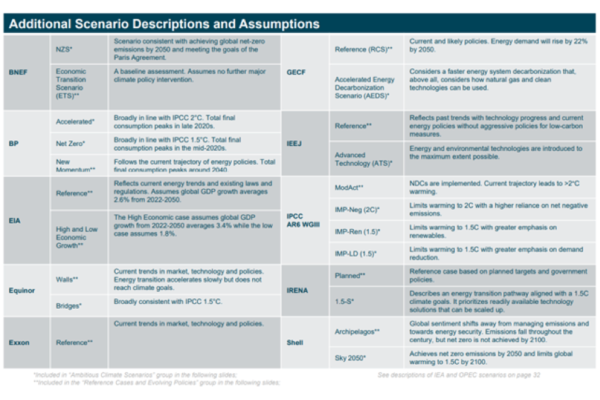

To get an idea of how the energy the EU transition can evolve, a comparison between the main energy scenarios is useful. The new IEF Outlooks Comparison Report offers a comparison between the IEA and OPEC scenarios and the underlying methodologies, placing them in the broader context of outlooks produced by other major industrial organizations and market players.

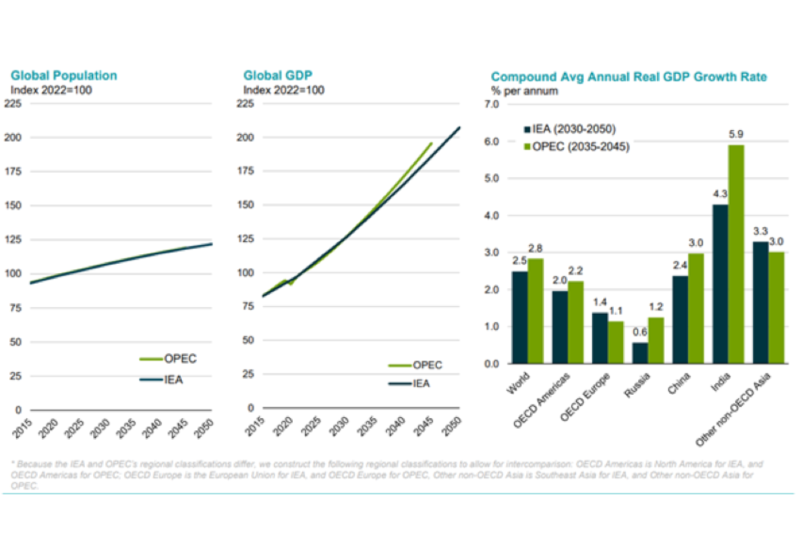

If we take a look at decarbonization scenarios up to 2045, both the IEA and OPEC assume that global GDP will double by 2050 and that the world population will grow by more than 20%.

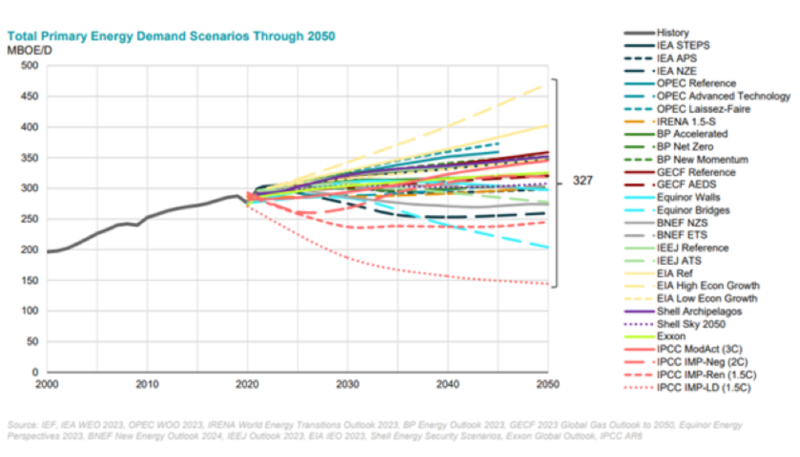

Three of the six reference scenarios show robust growth in primary energy demand. Under most scenarios, renewable energy is expected to more than double, and 4 of the 6 scenarios show that fossil fuels will account for more than 50% of primary energy in 2045 (up from 80% in 2022). Of the scenarios that envisage the achievement of the Paris Agreements, only the Net Zero Emission (NZE) scenario envisages a sharp decline in the demand for primary energy (15%) by 2045. All scenarios envisage the growth of renewables, hydroelectric, biomass and nuclear, within a range of from 95 to 224%. The ‘Renewables + nuclear’ share goes from ~20% in 2022 to 32%-78%. In the NZE scenario, the “other renewable sources” share goes from 3% to 42% in 2045, with solar increasing from 1% to 23% and wind increasing from 1% to 14%. Oil demand is expected to grow in 4 of the 6 scenarios, led by growth in non-OECD countries. Natural gas production will grow until 2030 in three of the six scenarios, also led by non-OECD countries. However, coal demand will decrease in all scenarios.

To outline where the consensus lies regarding the future evolution of the transition, IEF proposes the comparison of the IEA and OPEC projections with 23 other energy scenarios developed by 10 actors.

71% of all scenarios analyzed show end-of-period primary energy demand at higher levels than in 2022. Scenarios modeling more ambitious climate policies show a decline or plateau in energy demand.

The range between the high and low demand forecasts to 2050 is extremely wide, at 327 million bep/d, 8% larger than the entire 2022 demand. Scenarios in line with Paris show demand stabilizing o decreases from current levels, while most reference cases show demand growth above 15% by 2050.

Fossil fuels will still account for more than 50% of primary energy demand in 2030 under all scenarios examined.

In more than half of the scenarios, fossil fuels represent more than 50% of total primary energy demand in 2050: between 55-70% in many reference scenarios; between 15-30% in many of the net zero ones.

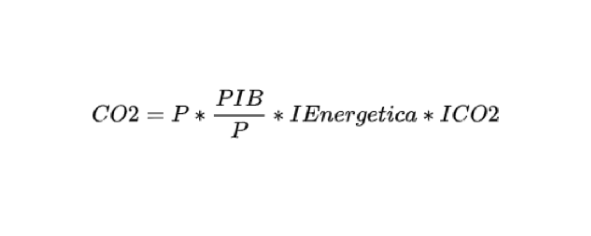

Without going any further, let’s contrast this information with the well rooted Kaya Identity that describe the factors that determine the human impact on climate:

Where P is Population, PIB/P is the Gross Domestic Product per capita, I Energética is energy intensity (MWh/$), and ICO2 is the Carbon Intensity (kgCO2eq./$). In all the scenarios proposed above, population and GDP continue to grow, while global primary energy demand in most scenarios raise 15% by 2050. In the light of these data, we can safely admit that the EU decarbonizations plans are exceptionally ambitious and far more optimistic than those envisaged by all the mayor technical organizations researching on energy transitions. But even in the case of an exceptional, massive deployment of renewable energy, like the one proposed by the European Commission, it seems clear that a continuous, consistent increase in population and GDP, as well as the primary energy demand vital to keep this new population out of poverty, will jeopardize global, and European, decarbonization plans, to say the least.

GDP, in fact, is one of the drivers of emissions: as the world gets richer, more people can access electricity consumption, or increase demand for heating, transport and other goods and services that require energy inputs (for 80% fossil type). On top of that, we are currently in a delicate phase of development on a global level where around four billion people, especially in the emerging Asian economies (among which India stands out), have reached an income level of between $2,000 and $20,000 Annual GDP per capita. This income drives up the demand for fossil fuels exponentially. Greater purchasing power implies a greater demand for transport (of people and things), a meatier diet, the consumption of more industrial goods and services. It fuels urbanization and the desire for greater comfort in the residential sector. It therefore seems that fossil fuels, like it or not, will be necessary to support our economies for decades to come.

Some final, uncomfortable reflections

We are now halfway between Kyoto, where the decision was made to prevent further dangerous temperature increases, and 2050 when the global energy system should be decarbonized –- a momentous divide to judge the progress, or the lack of it.

Our record so far is gloomy. Contrary to common impression, there has been no worldwide decarbonization –- just the very opposite as the world has become much more reliant on fossil carbon. Numbers are clear. All we had managed to do halfway through the intended grand global energy transition is a small relative decline of fossil fuel’s share in the world’s primary energy consumption, from nearly 86% in 1997 to about 82% in 2022. Of that approximately 18% non-fossil, wind and solar represent 4% more or less; the rest comes from nuclear, hydroelectric and biomass. However, this marginal relative retreat has been accompanied by a massive absolute increase of fossil fuel combustion: absolute consumption of coal, oil and gas, and relative carbon dioxide emissions, increased by 69%, 47%, 83% and 57% respectively compared to 1990 levels, and in 2022 the world consumed nearly 55% more energy locked in fossil carbon than it did in the year 1997. It is true that absolute cuts in carbon emissions took place in large economies such as the EU (-23%) and the US (-9%), but they were far surpassed by massive absolute gains in the world’s two largest industrializing nations –- China’s emissions rose 3.3 times, India’s three times –- as well as in the Middle Eastern hydrocarbon producers (Saudi emissions rose 2.3 times) and in other smaller emitters.

European decarbonization road map has weak foundations in technical and economic analyses done by major scientific organizations. The plan is both too ambitious and planned to be deployed on a too short time scale. Severing the EU’s reliance on fossil fuels is a desirable long-term goal, but one highly unlikely outcome that, for many reasons, cannot be accomplished either rapidly or inexpensively.

Michele Manfroni | Energy Expert

If you found it interesting, please share it!

Recent Articles