There is a fundamental dissonance at the heart of Europe’s energy transition. Electricity, by its very physical nature, is an intangible and indistinguishable commodity at the point of consumption. Yet the European regulatory framework has evolved towards an almost granular demand: the exact, verifiable and temporally precise certification of the origin of every unit of energy consumed.

This aspiration for absolute traceability, which might appear to be a purely theoretical exercise, is rewriting the rules of the game for energy-intensive industry. What was for decades a transactional process focused on optimising operational expenditure (OPEX) has been transformed into a strategic risk vector requiring the immediate alignment of Procurement, Sustainability and Finance.

Energy procurement is no longer simply a matter of securing a competitive forward price and acquiring an equivalent volume of annual certificates to satisfy corporate reporting requirements. Today, a procurement strategy that is misaligned with the physical reality of the electricity system constitutes a regulatory and financial vulnerability of the first order.

The Obsolescence of Annual Aggregation: RED III and the Guarantees of Origin Market

The traditional Guarantees of Origin (GOs) system operated under a premise of accounting flexibility. Traded in standard blocks of 1 MWh, it allowed corporations to adopt an aggregated, annualised approach. An industrial plant with a flat consumption profile (24/7) could operate overnight on energy from the residual grid mix and, at year end, acquire GOs from daytime solar generation to declare 100% renewable consumption. It was an administratively efficient mechanism, but one that generated a distorted representation of the physical reality of the electricity system.

The adoption of the RED III Directive in 2023, framed within the Fit for 55 package, marks the end of this flexibility. With the binding target of achieving 42.5% renewable penetration by 2030, the European legislator has recognised that genuine decarbonisation requires precise price signals. The directive introduces a substantial transformation by enabling the fragmentation of guarantees down to 1 Wh levels, laying the regulatory groundwork for hourly matching.

The operational implications are profound. The ability to offset consumption during hours without renewable resource through temporally uncorrelated certificates will be drastically curtailed. The GO market is already reflecting the tension of this structural transition, exhibiting unprecedented volatility.

Chart 1 — European Guarantees of Origin: Price Evolution (2019–2025) Source: AIB Annual Report 2024, Montel Energy, Pexapark | Prepared by: Magnus Commodities.

The historical evolution shows the transition from purely residual values (€0.35/MWh in 2019) to peaks approaching €7.80/MWh during the 2023 energy crisis. The recent downward correction, bringing prices below €1/MWh in early 2025, reflects a temporary supply surplus, but should not be interpreted as a return to the previous paradigm.

| The national transposition of RED III (2024–2025) and the progressive implementation of advanced granularity (2026–2028) anticipate a two-speed market: a premium segment for certificates with strong hourly and geographic correlation, versus a devalued segment for generic certificates that will lose validity under rigorous new audit standards. |

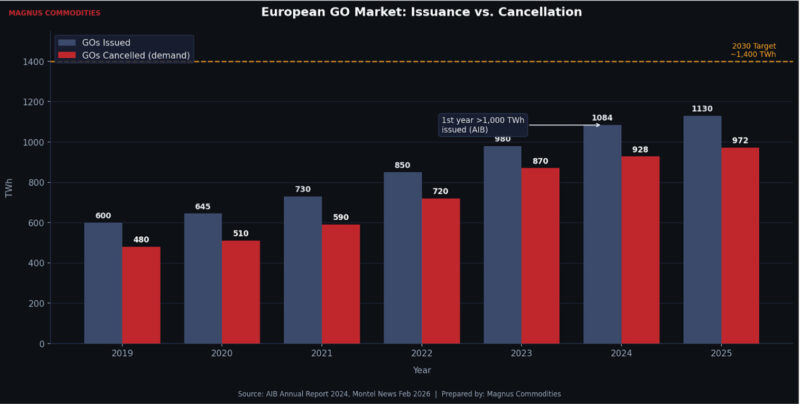

Despite price volatility, underlying demand maintains robust momentum. Data from the Association of Issuing Bodies (AIB) confirms that the certification machinery shows no signs of slowing.

Chart 2 — European GO Market: Issuance vs. Cancellation (2019–2025) Source: AIB Annual Report 2024, Montel News Feb 2026 | Prepared by: Magnus Commodities

In 2024, the volume of GOs issued exceeded the 1,084 TWh threshold for the first time in history, while cancellations the true indicator of corporate demand grew 5% year-on-year in 2025, reaching 972.5 TWh. This trend underlines that, regardless of the spot price of the certificate, the corporate need to certify energy origin follows an inexorable upward trajectory.

The Convergence of Reporting Standards: The Tightening of the GHG Protocol

In parallel with regulatory pressure on the generation side, corporate accounting frameworks are undergoing the most severe revision in a decade. The GHG Protocol, the de facto global standard for emissions measurement, is in the midst of a deep update to its Scope 2 guidance.

The proposals currently being consolidated, with final publication expected in 2026, introduce criteria that eliminate the ambiguities of the past. The requirement for strict temporal matching, the imposition of rigorous geographic boundaries limiting the transfer of attributes between non-interconnected markets and, fundamentally, the additionality requirement, are transforming the sustainability reporting landscape.

It is worth dwelling on the concept of additionality, as this is where many current corporate strategies present their greatest vulnerability. The new standards will require companies to demonstrate that their energy procurement has directly contributed to the addition of new renewable capacity to the system, invalidating the practice of purchasing certificates from hydroelectric plants amortised decades ago. For Sustainability departments, this represents a critical transition: the objective is no longer the mere completion of an annual report, but the auditable guarantee of the environmental integrity of the procurement strategy. Contracts signed today under yesterday’s rules risk becoming a reputational and regulatory liability of considerable magnitude.

The Internalisation of Climate Risk: The Imminent Impact of CBAM

If the modifications to the GHG Protocol affect corporate reputation, the Carbon Border Adjustment Mechanism (CBAM) directly impacts industrial economic viability and competitiveness.

Following a transitional phase launched in 2023 focused exclusively on reporting obligations, 1 January 2026 marks the entry into force of the mechanism’s economic phase. Designed to mitigate the risk of carbon leakage, CBAM will equalise the cost of CO₂ emissions between European production and imports from third countries.

The complexity lies in the calculation methodology. Electricity consumed in the manufacturing processes of CBAM-covered goods steel, aluminium, cement, fertilisers, among others becomes a critical component of the final product cost. In the absence of verifiable and traceable primary data demonstrating the use of decarbonised energy, the regulation imposes the application of default emission factors. These factors, calculated on the least efficient averages of the country of origin, are explicitly designed to penalise.

| Annual aggregated certificates will no longer be recognised as sufficient proof of renewable consumption under CBAM. For Finance, energy transcends its status as an operational cost to become an element of direct regulatory exposure and commercial margin risk. |

The Reconfiguration of the PPA Market: From Exuberance to Technical Complexity

Faced with this landscape of escalating demands, long-term Power Purchase Agreements (PPAs) have positioned themselves as the preferred hedging instrument. By linking corporate consumption to a specific generation asset, PPAs offer long-term price stability, guarantee the additionality required by new standards, and provide the traceability needed to mitigate CBAM exposure. However, the maturation of the European PPA market is revealing the frictions inherent in the mass integration of intermittent renewables.

Chart 3 — European Corporate Renewable PPAs: Contracted Capacity (GW) Source: Wood Mackenzie Apr 2025, Pexapark, SolarPower Europe Mar 2026 | Prepared by: Magnus Commodities

Following a period of sustained growth that culminated in a record 18.9 GW of contracted capacity in 2024, the market experienced a significant contraction of 31% in 2025, retreating to 13.1 GW. This correction does not reflect a lack of corporate appetite, but rather an exponential increase in the complexity of contract structuring.

The macroeconomic environment, interest rate volatility and inflationary pressures in the developer supply chain have complicated project financial close. More significantly, the demand for hourly correlation is forcing a renegotiation of profile risk allocation. Matching the intermittent generation curve of a solar or wind farm with the flat consumption profile of an industrial facility requires baseload structures or shaped profiles that substantially increase the risk premiums demanded by offtakers.

The viability of these transactions today requires a level of analytical sophistication and data processing capability that exceeds traditional procurement management tools. Hourly monitoring, load curve forecasting and dynamic hedging management require advanced technology platforms. Without robust digitalisation infrastructure, corporations operate with a critical information deficit in a market that does not forgive inefficiencies.

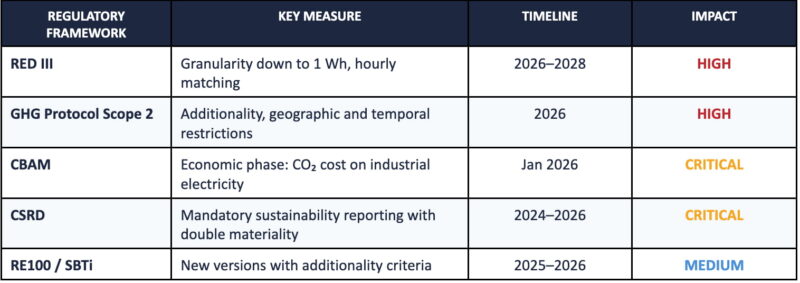

The Regulatory Horizon: The Convergence of Mandatory Compliance

The short and medium-term outlook demands an unprecedented capacity for adaptation from industrial corporations. The European regulatory calendar configures a scenario of maximum normative density.

Chart 4 — The Regulatory Complexity Map: Key Milestones 2022–2030 Source: European Commission, WRI, SBTi, RE100 | Prepared by: Magnus Commodities

Within a window of just 36 months, industry must absorb the simultaneous impact of the Corporate Sustainability Reporting Directive (CSRD), the national transposition of RED III, the economic activation of CBAM, and the implementation of new guidelines from the GHG Protocol and the Science Based Targets initiative (SBTi).

The most significant underlying trend in this timeline is the absolute convergence between voluntary standards and mandatory regulation. The traceability and additionality practices that until recently defined voluntary climate leadership are rapidly transmuting into minimum legal compliance requirements. There is no longer a meaningful distinction between choosing to be green and being legally required to be so.

To this regulatory density is added an emerging technical challenge: the problem of double counting at the product level. As impact analysis shifts from the corporate level to the product level through tools such as Life Cycle Assessment (LCA) and Environmental Product Declarations (EPD) the management of energy attributes becomes critical. The cancellation of a Guarantee of Origin to claim the renewable attribute, if that energy simultaneously remains in the residual grid mix used by third parties, generates a duplication of the environmental benefit that the CSRD’s new reporting obligations will expose with complete transparency, undermining the credibility of supply chains.

Towards Operational Coherence

Energy procurement in the European market has definitively moved beyond its phase of one-dimensional price optimisation. The new paradigm demands a transition from a logic grounded in flexible accounting instruments towards a model based on physical coherence, temporal correlation and strict verifiability.

In the second half of this decade, competitive advantage will not rest exclusively on access to renewable energy volumes at competitive prices. The differentiating factor will be the corporate capacity to demonstrate, with analytical precision and data consistency, that energy has been consumed in a real, traceable and verifiable manner, simultaneously meeting additionality requirements and reporting standards.

This structural transformation requires dismantling departmental silos. Regulatory and financial resilience demands an integrated strategy in which Procurement, Sustainability and Finance operate under a unified decision-making framework, supported by real-time data management capabilities. In today’s energy environment, the inability to adequately trace and certify the origin of consumed energy represents an economic risk that no industry can afford to assume.

If you found it interesting, please share it!

Recent Articles