In the past we focused in what derivatives markets are and in particular how OMIP (the Iberian electricity derivatives market) operates.

Nevertheless, the list of electricity markets in Europe is large (. It’s composed of a group of regional markets, which are more or less physically connected. These markets operate under the umbrella of the Electricity Regional Initiative launched back in 2006 (by ERGEG – the European Regulators’ Group for Electricity and Gas – now replaced by ACER – the Agency for the Cooperation of Energy Regulators) introduced to begin the transition into a single, integrated energy market. Each of the 7 regions is monitored by a different entity and a vital part of their unification work is to help establish wholesale markets for electricity.

The most relevant exchanges operating in these regions (and which increasingly overlap their products) are organized in an Association called the EUROPEX – The Association of European Exchanges. At the date of this article, EUROPEX had 27 members, a list of which can be found here. Of these members, many focus only in day-ahead markets (a.k.a. spot markets) or only in the trading of gas. Apart from OMIP, the ones which operate in electricity derivatives are:

EEX – European Energy Exchange

The EEX was established in 2002 and is located in Leipzig (Germany). It’s the result of a merger between the German power exchanges in Frankfurt and Leipzig. Since then it has evolved from a local power exchange into the leading energy trading platform in Europe, a fact well seen by their 147% increase in Sales Revenue in the period 2014/15 (from 77 to 190 million €). In this period the traded volume in power increased from 1570 to 2537 TWh – more than 4 times the total energy consumption of Germany in 2015.

ICE – Intercontinental Exchange

ICE launched in the year 2000 with an electronic trading platform and has grown non-stop since then, culminating in 2013 with their acquisition of the New York Stock Exchange. Their headquarters in Europe is located in London.

GME – Gestore Mercati Energetici

GME is a company wholly owned by the Ministry of Economy and Finance of Italy, and operates according to guidelines given by the Country’s Ministry of Economic Development and the electricity, gas and water regulator. As part of the process of liberalisation of the electricity sector, GME operates a forward market (MTE).

NASDAQ OMX

NASDAQ, like ICE, is active in every capital market. In 2007, NASDAQ merged with OMX (a leading exchange operator in the Nordics), and changed its name to NASDAQ OMX Group. In 2013 the group acquires Thomson Reuters’ investor relations, public relations and Multimedia Solutions businesses. NASDAQ is also a strong player, particularly in the Nordic System. Although their products encompass several countries, in 2015 the market report indicated trading only in Nordic, German and UK products.

OPCOM – Romanian Gas and Electricity Market Operator

The Romanian Power Market Operator – Opcom S.A. was established in 2000 based by Government Decision, as a joint stock company subsidiary of the Romanian Transmission and System Operator – Transelectrica S.A. and fully owned by it. Both the Romanian electricity and auxiliary services wholesale market are administered by Opcom S.A.

PXE – Power Exchange Central Europe

PXE is a subsidiary of the Prague Stock Exchange and was established in July 2007. It offers trading in Czech, Slovak, Hungarian, Polish and Romanian electricity.

Nevertheless, not all markets are created equal. By the sheer magnitude alone of the products they offer one can begin to feel that difference, but let’s look into each one in particular and compare their performance and prices.

Fig 1- Comparison between the market entry barriers vs. traded volume

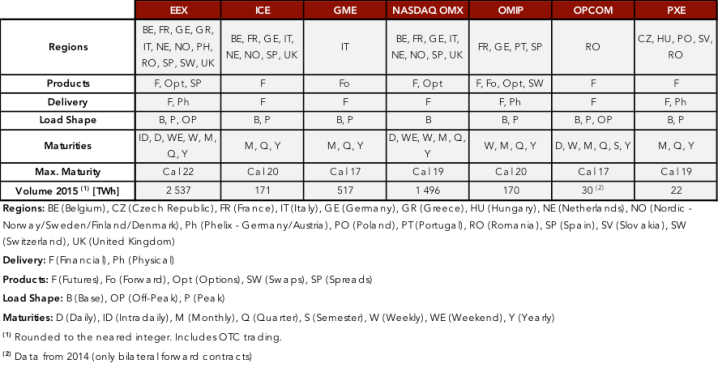

Enter Table 1 – Product Specifications of the main electricity derivative exchanges in Europe

MEANWHILE IN THE IBERIAN PENINSULA…

After the 2013 problem in these types of market in Spain (which affected the independence of the system), i.e. the Government’s intervention in the CESUR auction (which defined the prices for the domestic consumers for the next quarter) in the last quarter of that year, by which the Ministry of Energy cancelled the results of said auction, with the corresponding loses for the traders which took positions and had to undo them at a loss, 2015 was also a rough year for OMIP.

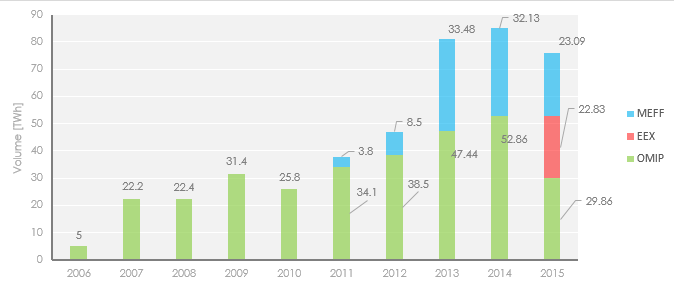

There was a great loss of players in the market. Although energy demand only fell by 0,84% in the past year, the traded volume in this exchange fell 43,5% to only 29,8TWh while the OTC volume fell by 49,2% to only 139,96TWh.

This forced OMIP’s management to search for new products, culminating with the introduction this year of German and French Futures. In the 2015 report, OMIP’s presidential board stated they intended to introduce Italian and natural gas futures as well.

This loss is most likely due to two factors: the first is the dropping-out, by some banks and funds, of these commodity markets and the second, and perhaps most important, is the introduction of Spanish futures in other European Exchanges – in particular EEX since August 2015 – which created a flight of traders, making a great entry into the market, with a debut share almost the same as the remaining market players as can clearly be seen in the next chart.

Apart from this, OMIP isn’t the only Iberian exchange trading in power futures. In March 2011, MEFF (the Spanish Market for Options and Financial Futures) launched MEFF Power – their electricity branch for the Spanish Peninsula. This branch saw spectacular growth in 2013. At the end of last year, MEFF had 109 registered participants against 58 in OMIP.

Although the entry barrier in OMIP is lower than MEFF (12.000€/year in the former against 16.000€/year in the latter), MEFF has a far more diversified portfolio and the transaction fees in MEFF are substantially lower, with a fee for Monthly, Quarter and Calendar products of only 0.0037 €/MWh below 2TWh/month and 0.0025 €/MWh above this threshold – which is almost half of those presented by OMIP and very competitive when compared to other European Exchanges.

Fig 2 – Traded Volume in Spanish Power in TWh in OMIP, MEFF and EEX

It will be interesting to follow this year’s evolution.

Hugo Martins | Analyst

If you found it interesting, please share it!

Recent Articles