The worldwide natural gas market experienced a significant upheaval in 2022 when Russia drastically reduced pipeline deliveries to Europe. This created exceptional pressure on supply and led to a global energy crisis. However, Europe managed to surpass historical storage averages in their underground gas reserves due to a variety of targeted policy measures, a sharp decrease in consumption, an accelerated deployment of renewables, interconnections, and sustainable technologies to enhance strategic autonomy. Nonetheless, the primary factor for this achievement was a record-breaking inflow of liquefied natural gas (LNG).

What is it?

LNG, as the name suggests, is natural gas that has been transformed into a liquid state. The attractiveness of LNG lies largely in its flexibility, as it can be imported even without pipelines, simply by using tankers that transport it to import terminals, where it is processed and made ready for use.

Importing LNG is a way for the EU to diversify its suppliers and routes for natural gas, which is especially important in the context of the EU’s plans to reduce its dependence on Russian gas imports.

Finding new alternatives

The REPowerEU plan proposed that member states secure supplies from their traditional partners and explore diplomatic avenues to engage new ones, sometimes competing with emerging economies and jeopardizing their energy supply. To make diversification possible, Europe turned to major energy producers, particularly those in its neighborhood.

The role of the US was crucial in overcoming the winter of 2022, both due to the significant increase in exports to Europe, which have more than doubled on an annual basis, and its assistance in convincing other countries to release cargoes already contracted with other customers.

Qatar was another key player. Initially, responding that its production was committed to long-term contracts with Asian customers and that it had little spare capacity to sell on the spot market, then opened the doors to negotiating longer-term export agreements – specifically, for after 2025. In March 2022, the Italian Foreign Minister, Luigi Di Maio, and the German Energy Minister, Robert Habeck, traveled to the Gulf to secure the deal.

The approach to Algeria and Morocco has also been encouraged, and there has been renewed interest in Iranian gas as well, although as a long-term option, due to their abandoned or nonexistent energy infrastructure, that makes a quick solution to Europe’s energy crisis impossible.

LNG Boom

The response of the gas markets, with European indices offering much higher prices than Asian ones, made it possible to attract LNG carriers to EU regasification plants.

LNG imports reached record highs in 2022 making the EU the world’s largest importer of LNG. In 2022, EU LNG imports reached 14.9 billion cubic feet per day (Bcf/d), which was a 65% increase compared to 2021 and a total of 24% of all LNG traded last year. France was the largest EU LNG importer, ahead of Spain and Belgium. Europe’s role in the LNG market changed dramatically from a passive and flexible LNG sink to a direct and aggressive competitor.

Source: U.S. Energy Information Administration. 1 Bcf = 1,000,000 MMBt.

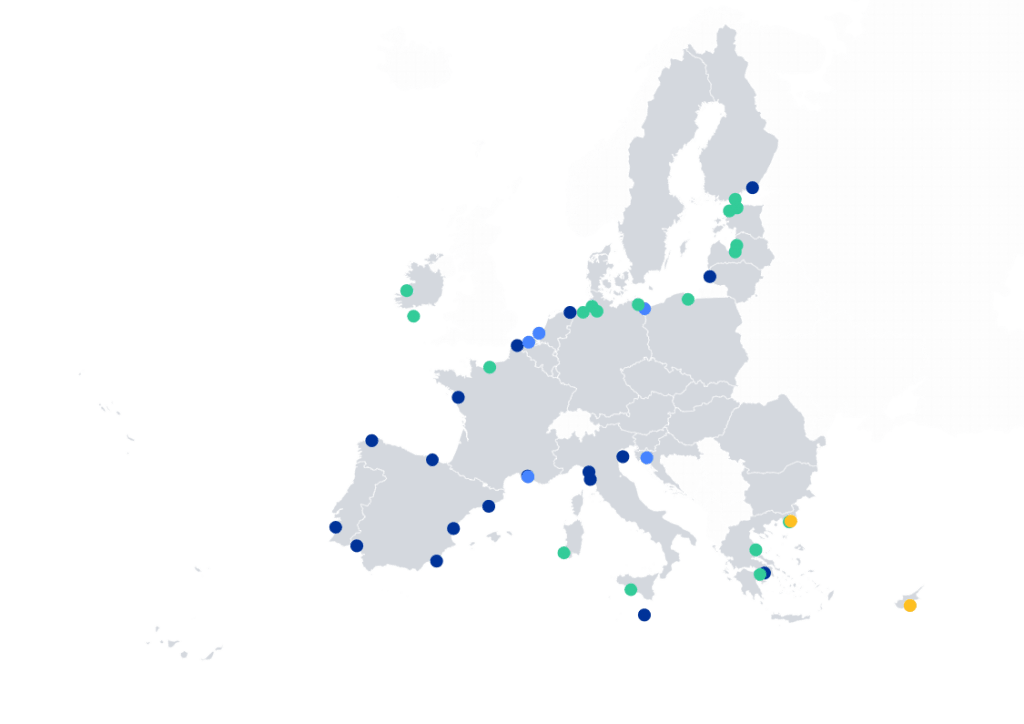

LNG infrastructure in the EU

With the challenge of diversification overcome, there was a new challenge: increasing total LNG import capacity was fundamental but access to LNG infrastructure in the EU was not uniform.

EU launched many projects to further develop the LNG infrastructure. Most of the new regasification projects consisted of chartering Floating Storage and Regasification Units (FSRUs) and by building pipelines to transport regasified natural gas to connecting pipelines onshore. Other regasification projects consisted of expanding capacity at the existing onshore terminals and implementing upgrades to increase existing terminals’ throughput.

In 2022, approximately 2.0 Bcf/d of the new and expanded LNG regasification capacity has been added in the Netherlands, Poland, Finland, Italy, and Germany, and in 2023 an additional 3.5 Bcf/d of new capacity is expected by the end of the year.

Title: LNG infrastructure in the EU, 1S 2022.

The new EemsEnergy terminal in the Netherlands (0.8 Bcf/d capacity) consists of two FSRU vessels and received its first import cargo in September 2022.

A new FSRU terminal at Wilhelmshaven Port in Germany (0.7 Bcf/d capacity) has been completed in November 2022, as well as three other new FSRU terminals, which will cumulatively add 1.4 Bcf/d of regasification capacity at Lubmin, Brunsbuttel, and Wilhelmshaven and are already online.

Finland and Estonia jointly developed an FSRU terminal in the Finnish port of Inkoo, which adds 0.5 Bcf/d capacity and went online in December 2022.

Italy developed an FSRU terminal near the port of Piombino, which adds 0.5 Bcf/d of capacity and went online in March 2023.

Poland will expand capacity at the existing LNG regasification terminal at Świnoujście by 0.2 Bcf/d to reach a total capacity of 0.8 Bcf/d by December 2023.

France will add 0.4 Bcf/d of regasification capacity using an FSRU vessel called Cape Anne at Le Havre port, which is expected to come online in fall 2023.

Greece will bring online an FSRU vessel at Alexandroupolis port by the end of 2023, with 0.5 Bcf/d of regasification capacity.

Overall, according to the Energy Information Administration (EIA), the EU and the UK are expected to increase their combined LNG import capacity by 34%, or by 6.8 Bcf/d, by 2024 compared to 2021.

Asia, the main threat

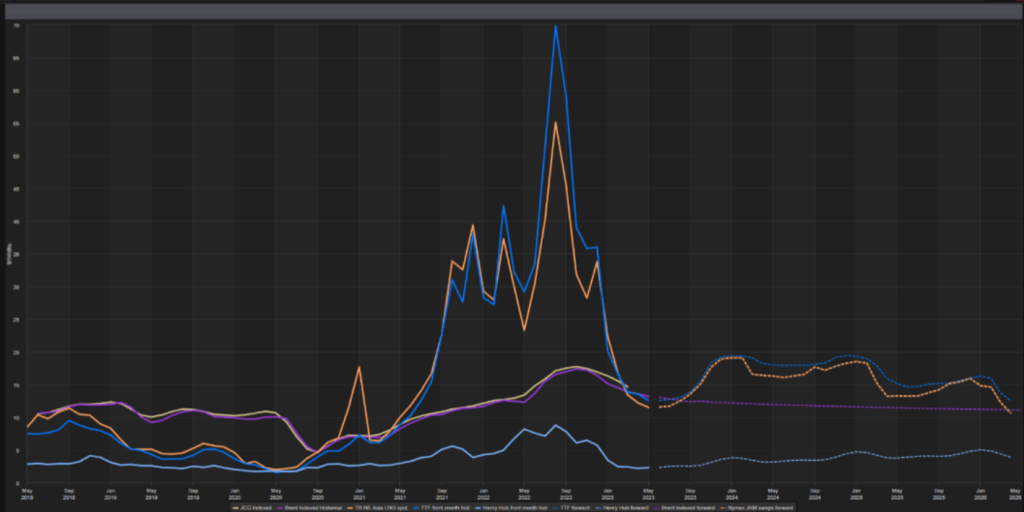

With record LNG imports last year, gas and LNG prices averaged a record $40/mmbtu, and many companies were forced to rethink their needs.

Title: LNG (Spot and JCC-Indexed, TTF and HH Prices). Source: Reuters. Note: 1 MMBTU = 0.293071 MW.

Much of Europe’s LNG imports were helped by lackluster demand in Asia, where China experienced an unusual drop in gas consumption amid slowing economic growth, while most of South and Southeast Asia simply could not afford the skyrocketing LNG spot prices, being forced to switch to alternative fuels and reduce their production to try to limit their exposure to the spot market.

So, last year Europe won the competition with Asia.

But today the situation is very different. Gas prices in Europe and LNG prices worldwide are now trading below $15/mmbtu. If this trend continues, European and Asian companies will have a strong incentive to switch back to gas instead of other fuels.

And we cannot forget that China is one of the biggest economies, responsible for almost one-fifth of global oil consumption and overtook Japan in 2021 as the world’s largest importer of LNG.

If the Chinese economy recovers quickly, it could put commodity and gas prices under intense upward pressure and keep inflation high in Europe. This would reignite competition, which could divert tankers, as it is already happening inside Europe, throw Europe’s plans into turmoil and trigger another global energy crisis.

So, the question for 2023 and beyond, that we all hope to see answered is, what plan does Europe have to continue to outperform Asia in LNG supply once Asian demand starts to recover, without compromising industry demand and its carbon neutrality commitments?

In the meantime, let’s hope that “May the weather be with us”.

If you found it interesting, please share it!

Recent Articles