Every company seeks to lower costs more efficiently. One of them is the energy: in Spain seems to be above our European neighbors. Since 2012, the price in the future wholesale market has traded between 10% and 20%, on average, higher than countries such as France and Germany. The energy production mix causes this difference, and consumers can do little about that. Therefore, it is quite challenging for Spanish consumers to reduce this cost compared to other countries in Europe.

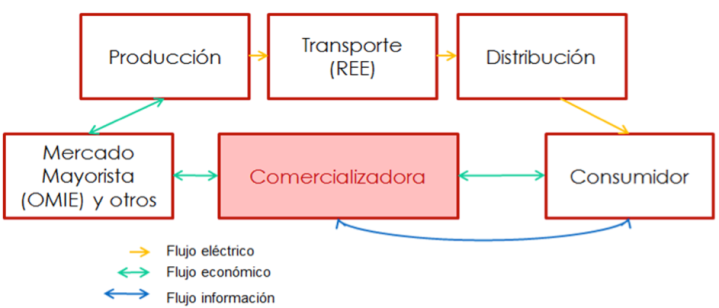

Where they can take decisions is on the other side of the chain. We mean the Energy supplier side. The standard structure in which the large majority of consumers participate in the power supply is:

In the latest report of the retail market, the CNMC explains that in Spain there are 167 active suppliers of energy, far away from the 1,050 who already had Germany in 2012. Moreover, even having so many suppliers, the Spanish market still presents a significant concentration ratio. According to data from Eurostat, 80% of electricity sold is concentrated in just 4 companies known as traditional marketers: Endesa, Iberdrola, Gas Natural Fenosa and E.ON:

% Market Share vs. Incumbent Suppliers by Country in 2013

In this graph, the bars represent the accumulated percentage of the market share (left axis) and the points are the number of suppliers concentrating the market share (right axis). As you can see, Spain (ES) has a long road ahead against countries like Germany (DE) where the main traders do not reach the 50 percent market share.

In this situation, consumers can find different trading strategies, such as joining in partnerships and gain strength in fixed-price tenders, or may tend towards electricity products that reduce supplier’s margins (indexed products). But others are opting to eliminate directly the supplier of the equation: being a Direct Consumer or, in case of several companies, being direct representative of several direct consumers. In this mode you buy your own electricity and operates directly with REE (System Operator); with OMIE (Market Operator); OMIP (Exchange) and even electricity producers or traders. Therefore, direct consumer pays only the actual cost of the wholesale energy market (plus System Operator tasks and taxes) and eliminates the supplier’s fee as intermediary; by taking in charge the risks and tasks of their former suppliers.

There is the direct Consumer figure and the Representative figure. Difference is: the direct consumer buys only the electricity for sites under the same Vat number while the representative figure allows to group different Vat number sites thus uniting various direct consumers under one umbrella. Many business groups opt for the latter figure where the representative consumer is usually a direct part of the group.

Moreover, according to the Administrative Register of Distributors, Suppliers and Direct Consumers updated July 1, 2015, there are today in Spain there are 123 companies discharged as direct consumers on the wholesale market but only about 66 companies are actively buying . How can it be possible that 57 direct consumers are not buying? The answer lies in the 27 representatives who cover the rest of direct consumers and even some traditional suppliers, which also offer representative services.

This representative can make the purchase either jointly, known as indirect representative, or individually for each direct consumer, being a direct representative. The difference between direct and indirect representative remains in how the direct consumer inter-acts with OMIE and REE for the purchase and payment of energy costs.

To sum up, the ways to act as a direct consumer with the electricity market are:

Besides avoiding the supplier’s margin by directly access to the wholesale market, the consumer will not only buy electricity on the daily market but also in the intra-day markets. These markets consist of 6 additional sessions that allow them to buy or to sell electricity that was not contemplated in the initial purchase for the daily market. These sessions can improve the energy management by minimizing the differences between what was expected to be consumed in the next day and what is actually consumed in that day. By reducing these differences, the consumer reduces the detours cost that REE will apply. Even more, the daily market prices can be improved by acting in the intra-day markets.

However, to operate properly technical support is required or at least a:

– Telemetry equipment for charting the consumption in real time and act in intra-day sessions accordingly

– Market analysis model and purchasing strategies for pricing whether daily, intra-daily or fixings´ futures market or even bilateral contracts.

– Service to process information and manage interactions with OMIE and REE.

In case of not contemplate these requirements, the company would run the risk of missing the benefits of the direct consumer model and even ending up paying more than with the standard supplier contract.

One of the main appeals of this new figure is the fact that they can directly avoid the city tax (1.5% on the total cost of the final invoice) that is about 1 €/MWh. This rate stems for the private use or special use of the local public domain.

To ask whether this model is appropriate, you must weigh the pros and cons. Not only it requires an effort in the direct management of the purchase but also requires a financial capacity. For instance, both OMIE and REE, through MEFF, require Guarantees as a way of prompt payment: OMIE gets payed every week and REE every 15 days. From a financial point of view, it is a major change that not many want to put up with.

The figure of direct consumer is unusual because it has favorable and unfavorable points, and in some specific cases the pros wins the cons. That is why many companies where energy is small piece of the P&L do not even consider this buying model.

However, when energy is one of the recurrent costs in the budget meetings, is right there where managers should make this reflection: Is it worth? With this, we ensure at least that all possible alternatives to manage energy costs have been analyzed.

Magnus Commodities believe in innovation and the necessity of companies to look for new ways of buying energy, putting in a balance risks and benefits to that before taking a decision. Our aim is to act as Energy counselors and explain to our clients all the different options.

Clearly, the Direct Consumer figure is not valid for every Company, it has to be understood what it means. European companies are used to high cost of the Energy components, already incorporated in their teams high qualified professionals to minimize those impacts.

Taking into account Europe is heading towards a unique Global Power Market, it will be very interesting to keep track of the effect on the buying Methods in each territory and how quick we will be shifting from old models to the new ones, still to come.

Marta Merodio | Energy Consultant

If you found it interesting, please share it!

Recent Articles