Four years ago the IEA, introduced the concept of “the golden age of gas”. Nowadays there is no place where this expression seems more relevant and real than Asia, where a bright future seems to await this commodity, and where its demand in 2035 is estimated to equal that of USA.

The LNG industry has looked for a long time to Asian markets such as Japan, South Korea and Taiwan, high-growth markets, eager to sign long-term sourcing contracts.

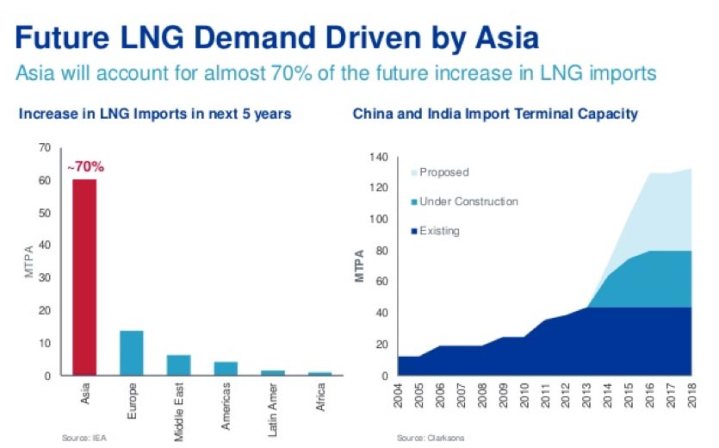

But regardless of the growing demand, Asian countries seem to be stopping their march toward gas consumption because of the premium price they have to pay.

The reasons behind this price supplement are varied but can be summarized in four main points:

- The prevalence of long-term gas contracts often indexed to oil prices

- The difficulties encountered in ensuring the security of supply

- The low level of flexibility of the demand

- The absence of adequate spot markets at a regional level, reflecting the Asian balance between supply and demand.

The issue concerning the price of LNG in Asia is now becoming crucial in determining the future development of the global demand and supply logic, and at the same time setting the pace at which the continent’s markets will reach full liquidity and flexibility. To understand the evolution of this market it is necessary to analyze the two sides of the coin: the demand and the supply, where the latter can be divided into domestic production and imports.

Starting from the demand side, we can certainly say that the price is the key factor that can increase the spread of LNG, and currently there are two main issues affecting the diffusion of this commodity, including:

- The mechanism of oil indexed prices that make gas prices significantly higher than those traded through the hubs.

- The lack of flexibility in the supply of LNG, which often includes clauses of final destination and take-or-pays.

The indexation to oil, it is often more comfortable for suppliers, given that many of the development costs are related to crude prices. In addition, Asian suppliers see in the gas-regional markets, such as Europe, significant limitations, mainly due to: low levels of liquidity, possible prices manipulation by large market players, and high levels of volatility.

Most likely Asian countries will develop their hubs in the medium- long term. This process is essential to increase the levels of efficiency and transparency of their markets, and significantly reduce the premium price that Asian consumers currently pay for gas. Furthermore, the progressive development of the national gas hub, can substantially strengthen the bargaining power of Asian buyers, providing an additional price signal that could be used during the negotiations of long-term contracts.

On the supply side, the profound imbalance between the prices offered by Asian gas producers and the prices of the US import gas is evident.

The likely scenario for Asia over the next decade is a transition from oil indexed to HH (Henry Hub) indexed formulas, basically depending on the price of American gas, which is expected to absorb a large portion of Asian demand in the years to come.

But whatever the future holds, the aspirations of American companies, that in the wake of the shale gas success, made great plans for expansion, today come up against a hard reality:

- The fall of crude prices has dragged down also gas prices, while low coal prices and renewables development are contributing to the slower expansion of LNG

- The Japanese demand for gas is decreasing, after growing exponentially following the Fukushima disaster in 2011, when the closure of the nuclear reactors imposed a change in the generation mix of the country

- The entrance on stage of Australian competitors, that, on the heels of the American success, have invested more than 200 billion dollars for the development of major extraction projects.

The result is that the global production of gas has already reached the 250 million tons.

Given the increase in supply and modest expectations of demand growth in the short term, utilities are forced to reduce investment, operating in an opportunistic manner, focusing on the short term and avoiding long-term contracts. In any case, although mature buyers of gas such as Japan, Korea and Taiwan, may see reduced their gas demand, China and Southeast Asia continue their climb, becoming, thanks to the high regional prices, perfect countries for LNG exporters.

The two fundamental questions at the basis of the expansion of the LNG market in Asia are therefore the cost and level of flexibility.

To Entailing significant costs in the coming years will be:

- The development of new extraction projects, both for domestic production and exports.

- The cost of liquefaction and transportation of LNG projects

- The cost of alternative energy sources (such as coal), compared with the cost of gas and the price that end consumers will be willing to pay for both

Regardless of its abundance, gas seems to have been converted into an essential component of the global energy mix, as well as one of the best allies in the fight against global warming, replacing highly polluting fossil such as coal or derivatives of crude.

The growth in energy demand for this commodity implies not only competition from other fuels but also the need of a greater availability. A risky scenario, especially when you consider the low storage capacity of many Asian countries, and even more, looking at the poor capacity of inter-regional exports.

In order to conquer the Asian market, the LNG must therefore lose its status of “premium-fuel”, opting between three possible options:

- Keeping the oil-indexation, but with price curves characterized by lower slopes

- Focusing on HH (Henry Hub) indexation for, at least, a part of their contracts

- Include in the contracts the possibility to use a long-term spot price, once the Asian markets will be fully liberalized and with sufficient levels of liquidity

Asia is entering an era of much more efficient energy markets, with undeniable benefits in terms of security of supply, but there are still warning signs: the high price of liquefied natural gas threaten to curb the demand of those nations that are not able to afford the purchase of expensive gas and inevitably will end up opening the door to coal.

If Asian markets do not manage to increase the level of transparency of prices and will not invest in new production and facilities for the liquefaction of natural gas, the only way to move Asian investments from coal to gas will be a strong commitment to climate policies on low carbon emissions.

Maria Mura | Energy Consultant

If you found it interesting, please share it!

Recent Articles