As mentioned in previous M•Blogs, Europe is facing a major challenge as regards reducing emissions of greenhouse gases in the coming years, especially after the new commitments made at the UN climate summit held in December 2015 in Paris. Because of that, many countries have established specific measures aimed at promoting renewable energy and reducing coal consumption quotas, especially for electricity generation. However, the constraints of current market place, to some extent, are increasing the difficulty to meet such measures. Oil price drop since mid-2015 is still a key factor, with lower benchmark gas and coal prices in Europe, which makes the use of these technologies cheaper to power production. In addition, EUA allowances prices have fallen 34.5% since mid-2015, so they are not fulfilling their expected goal of discouraging burning coal.

Regarding power generation, Europe is betting on decarbonisation, towards renewables but also gas as a flexible, manageable and able to act in peak hours alternative, but which in turn is less polluting than coal. But, what factor may allow the change from intensive coal to gas in generation? The key is the profitability of each of these technologies.

The term used for the concept of gross margin of a power plant by burning gas in the sale of a unit of electricity is known as “Spark Spread“. In the case of burning coal, it is called “Dark Spread“. This margin is expressed in €/MWh and is calculated as the difference between the selling price of electricity and the burning costs of each hydrocarbon. Theoretically, operating and maintenance costs of the plant should be taken into account, but usually they are simplified by considering only the cost of raw materials and plant efficiency. In a generic way, efficiency coefficient values are usually around 36% for coal plants and 50% for gas (combined cycle application). Therefore, the calculation can be standardized as:

If you take into account also CO2 emission rights costs in each case, margins are called Clean Spark Spread (CSS) and Clean Dark Spread (CDS).

The carbon emission factor for a coal-burning plant is 2.5 times that of a gas plant. Therefore, a coal plant will face a higher cost to cover their carbon emissions to generate the same amount of electricity, since it is more polluting.

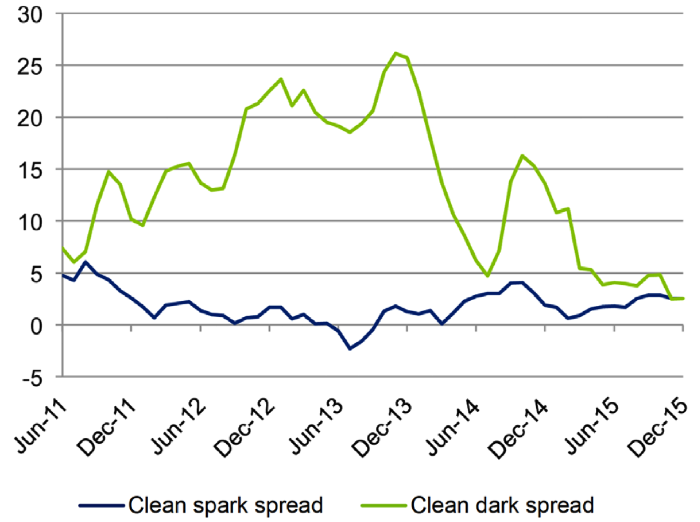

Despite this, historically, to generate the same unit of electricity, the cost associated in gas plants has been higher than burning coal, as you need less amount of coal to obtain the same energy. Hence, CDS are above of CSS values.

However, UK is faced with a new scenario. Like the other European hubs, NBP gas price has been declining since 2015. Although the international coal price has also fallen, increasing import costs by the weakness of the pound against the dollar has dimmed the fall. But certainly, the factor that is having greater influence in spreads is the establishment of a floor price on CO2 emission rights. Britain has established as a national goal to reduce CO2 emissions by 80% in 2050 compared to 1990 levels. To meet this goal, first they will cease burning coal generation by 2025, and they have set a carbon target price for 2020 at ₤30/tCO2, which will be achieved progressively each year. The difference between EU ETS prices and the annual floor price is covered by the so-called “support rate”, which must be supported by the generation.

This situation is leading to a substantial reduction in CDS, because burning coal involves a greater emission factor than gas. Since the beginning of 2016 we are seeing an increasing participation of CCGTs, displacing coal to peak hours. The difference between CDS and CSS has been declining, approaching equality.

CDS and CSS spot in UK (GBP/MWh). Source: Capital IQ

Carbon floor price, therefore, is very close to the so-called “switching price“, ie, the CO2price that allows that a change from coal to natural gas or vice versa is economically advantageous for a power producer. If the price of allowances exceeds the “switching price”, burning gas becomes economically more advantageous than burning coal.

But, does gas entered in UK to stay? The emission reduction target proposed by UK is ambitious, and if coal generation will cease in 2025, the country will also need to reduce gas share thereafter, fostering other technologies with lower levels of emissions, such as nuclear or renewables. The lack of government support to CO2 storage (Carbon Capture and Storage Technologies – CCS) also makes it more difficult. For that reason, although currently change in UK power generation model, companies cast doubt on the viability of investments in new CCGTs plants.

UK is an example of how government measures in the carbon market are causing a change in the country’s generation mix. Meanwhile, the rest of Europe is beginning to rethink the current allowance system, with the idea to start taking measures to allow increased prices after the sharp drop suffered since 2015. If we analyze the evolution of CDS and CSS in other European countries like Germany, what is observed is that the CSS has been increasing, reducing the gap with CDS. However, there is still a significant difference between them, compared with UK.

CDS and CSS spot in Germany (€/MWh). Source: Capital IQ

The sharp drop in carbon emission rights prices in Europe is making the reduction of coal share more difficult, only for market reasons. In fact, Germany has increased coal share from 41.53% to 42.20% in 2014 and Spain from 15.51% to 20.46%.

According to this change of model, Europe is beginning to take note of UK, and there have already been several initiatives to establish floor prices in the EUA system. Europe must take action if they want to meet their emissions reduction targets, encouraging market to let to a change in the energy mix.

Susana Gómez | Energy Consultant

If you found it interesting, please share it!

Recent Articles