A mix between favourable weather for renewable energy generation, an efficient grid management and a healthy interconnection participation resulted in the cheapest Spot prices ever experienced since the beginning of Spanish SPOT Market. SPOT average price was 32.79 €/MW at the end of the summer, which is historically the most expensive time of the year, putting the estimations setting the final average SPOT price of 2016 at 35€/MWh. One of the key drivers of this range of low prices was the increase of energy imported from France. What was not expected was that the key driver would become the key problem from what we have been experiencing since September. In just two months, the Spanish day-ahead prices rose (in average) 12 €/MWh because of the nuclear crisis in France that started in May and exploded 4 months later, dragging a lot of European countries with it.

Figure 1: OMIE 2015 vs OMIE 2016. Source: Magnus M·Tech

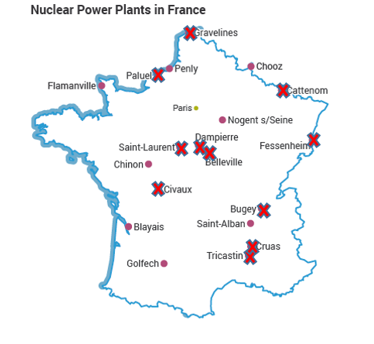

The France Nuclear capacity

France is the number 1 country in terms of nuclear energy production and development. 75% of all energy generated in France comes from nuclear power plants spread all over de country.

Its background goes back to 1974, when France decided to import nuclear technology to become more independent in terms of energy security. The heavy R&D investments made in this sector contributed to put France in the highest position as the nuclear energy leader until now.

With this strategy, not only France has one of the lowest levels of carbon emissions by amount of energy generated, counting with more than 90% of its energy mix emissions free, it also is the major electricity exporter in Europe, after an energy review, in 2010, by the International Energy Agency (IEA) affirmed that France should take a strategic role as provider of low-cost, and low-carbon base-load power for its bordering countries and not just generate nuclear energy for domestic purposes.

The state-owned electricity company EDF is the owner of the 58 nuclear reactors divided in 19 power plants spread across the country (figure 2). It is also involved in the recent approved nuclear project that is going to be developed in England, at Hinkley Point with a cost of 21 billion EUROS.

As the only operator of nuclear power plants, EDF was forced by the French Energy Regulator (CRE) to establish fixed prices to sell electricity, from 2014 until 2017, to allow more competition between all the energy suppliers that participate in the French market and to ensure that all the competitors would buy nuclear generated electricity from EDF, in order to the state company could recover the costs from the upgrades executed in the past years (55 billion Euros to extend the reactors’ lifecycle ten more years). The prices to be applied in 2014, 2015, 2016 and 2017 were, respectively, 42, 44, 46 and 48€/MWh. However, in 2015 the government decided to freeze the price at 42 €/MWh to maintain competitiveness against bordering countries like Germany.

Other hit in the EDF situation came in October 2014 when the Energy Transition for Green Growth Bill was approved by the National Assembly. This roadmap stated a need for France to decrease for 75% to 50% its nuclear capacity by 2025, along with the goal of emission reduction by 40% until 2030 and 75% until 2050, compared with 2012 levels.

The nuclear nightmare

As any power plant, nuclear power plants have maintenance periods that are dully scheduled having in mind all the supply/demand issues, in terms of loads and in terms of local, regional or national energy needs.

The EDF and, consequently, the French nuclear nightmare started in 2014, after a flaw was detected in the pressure vessels of the under-construction new generation EPR Flamanville 3. This finding, along with the phantom Fukushima, conducted to an investigation that led to an even more scary discover this May: 400 other sub-standard parts were identify and a lot of falsified quality control documentation! Even worst, many of the parts identified with flaws were already inside nuclear plants that were running.

ASN took immediate action and force EDF to put in march a plan of re-evaluation of most of the plants identified in the documents and with the broken parts installed. Since the beginning of 2016, 30 nuclear reactors were stopped, having been 11 already restarted until now. The remain 18 nuclear reactors still in maintenance correspond to up to 17 GW of energy capacity, which is 27 % of all nuclear capacity installed in France and 21% of Total French capacity.

Figure 2: Nuclear Plants in France. Source: WNA

According to the Figure 2, only 6 nuclear power plants all over France are working at full capacity, and some of them still have some outages scheduled between January and April of 2017.

Data recovered from Reuters shows that is expected that 13 500 MW is going to be restored until the end of 2016. And by the end of the second quarter of 2017 is expected that 57 860 MW or the equivalent of 91% of total nuclear capacity will be up and running.

Figure 3: Nuclear capacity restore evolution. Source: Reuters

The spread of the nightmare

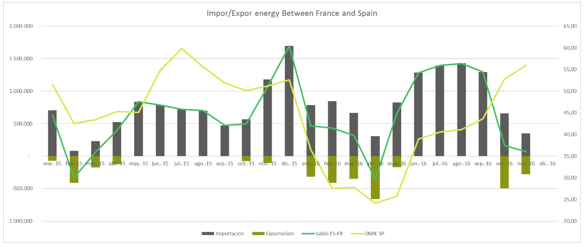

As commented before, France is the biggest energy exporter in Europe, sending large amounts of electricity to countries like, Spain, Italy, Germany and UK in a daily basis.

As we can see in the Figure 4, those exports help to a more stabilization and even more proximity of the prices all around France. So, as expected, these unexpected outages were not a benefit for anyone, specially to Italy, UK and, of course, Spain.

These three countries passed from net importers to Energy exporters, as demand for energy in France increased abruptly, especially with the beginning of the winter.

Looking at the Spanish case, it is quite clear the influence of the interconnection between the two countries. If we take a close look at the SPOT prices evolution between 2015 and 2016 we can verify that, bigger imports from France keep the OMIE at lower levels (difference between summer 15 and summer 16). Also, we can note that SPOT prices rebounds when the imports decrease (from September to November 16 when most of the current 20 of the nuclear reactors stopped).

Figure 4: Energy Imports/Exports between France and Spain. Source: ESIOS

Besides from the energy crisis generated all over the bordering countries, the absence of rain across Europe in the last months contributed for a significant fall on the water reservoirs, decreasing also the hydropower participation in the energy mix.

Focusing in Spain, SPOT prices were pushed upwards, first by the fall of renewable energy sources (since June) with special focus of hydropower and ultimately driven by the main subject of this article, which is amply visible from September to October.

Lower imports, along with low levels of water main reserves, forced Spain to rely on fossil fuels to supply its demand. Remembering that carbon is being traded at maximum levels (up to 60 $/ton) also supported the rise of the electricity prices in Spain and in other countries affected by France current situation.

Figure 5: Spanish Energy Mix Evolution. Source: ESIOS

CO2 emissions is another subject that should be considered here with all the buzz around the signing of the COP21 agreement and the need to cap and cut global emissions drastically and rapidly. The current scenario made countries to emit at yearly maximum levels, especially France, since it was forced to restart some coal power plants to try some price stabilization, being now emitting at levels registered 32 years ago.

Future notes

As the Figure 3 shows, by the second quarter of 2017 91% of the nuclear capacity in France should be running without problems and we all wish that this nightmare is solved ASAP. However, it raises a question about the UE dream of a Single Energy Market. To that goal achieve that kind of security and stability, an efficient and well connected energy grid must be a reality, connecting all the UE-members (and some non-members) to constantly balance the energy needs from any country any time. The nuclear crisis was, actually, a great test to the developments executed so far, once that, the interconnections were crucial to avoid major problems of shortages or even blackouts. However, other reason to a successful Singe Energy Market is to provide more competitivity and parity between the prices in the Euro Zone ensuring less costs to the final consumers. Well, this episode in France revealed a flaw in this scenario that needs to be reviewed in order to prevent that similar situations in the future, spread all over the countries involved in that bigger project.

Jorge Seabra | Energy Consultant

If you found it interesting, please share it!

Recent Articles