The Twilight of OPEC? Implications of the United Arab Emirates’ Exit

The recent decision by the United Arab Emirates (UAE) to leave the Organization of the Petroleum Exporting Countries (OPEC) and the OPEC+ alliance, effective May 1, 2026, marks a critical turning point in global energy geopolitics. After almost six decades of uninterrupted membership, the exit of the cartel’s third-largest producer raises fundamental questions about the future viability of the organization and the stability of oil markets.

This analysis breaks down the underlying factors of this historic decision and its short- and long-term consequences, based exclusively on data and context provided by recent industry coverage.

The Decline of OPEC’s Influence

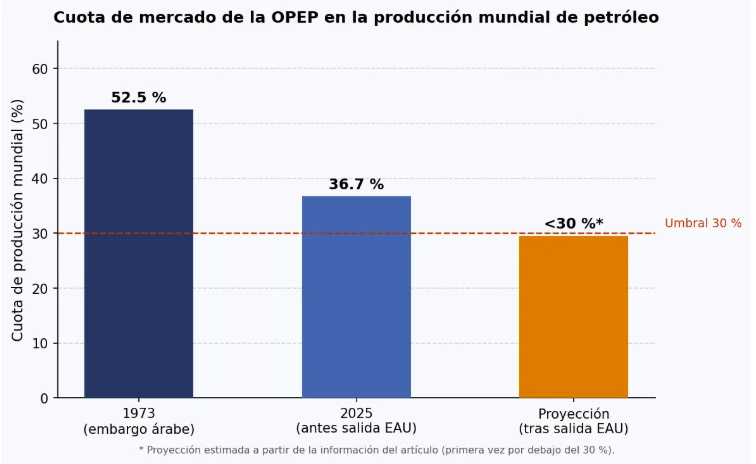

Since its founding in 1960 and its consolidation as a dominant geopolitical actor in the 1970s, OPEC has experienced a steady erosion of its market share. During the 1973 oil embargo, the cartel controlled 52.5% of global production. However, by 2025, this figure had dropped to 36.7%, driven largely by the rise of external producers, notably the United States.

The UAE’s exit exacerbates this trend. It is projected that, without the Emirati contribution, OPEC’s global share will fall for the first time below the psychological and strategic threshold of 30%.

This loss of specific weight is not an isolated phenomenon. It follows the previous exits of Qatar in 2019 and Angola in 2024, evidencing the organization’s growing difficulty in maintaining internal cohesion in the face of the divergent interests of its members.

The Reasons Behind the Break: Quotas vs. Capacity

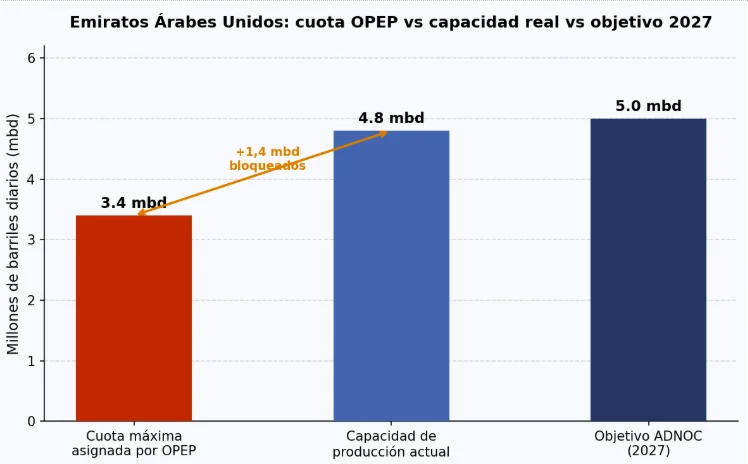

The main trigger for Abu Dhabi’s exit lies in the rigid production quota system imposed by OPEC. The UAE was assigned a production limit of between 3.2 and 3.4 million barrels per day (mbd). This restriction directly clashed with the expansion strategy of the national company ADNOC, which has invested approximately 150 billion dollars to raise its current production capacity to about 4.8 mbd, with the goal of reaching 5 mbd by 2027.

The obligation to keep 1.4 mbd of capacity idle represented an unacceptable opportunity cost for the UAE, forcing them to sacrifice state revenues vital for their economic development and diversification. The decision to prioritize the independent monetization of their reserves reflects a paradigm shift: from cartel solidarity to national profit maximization.

The Geopolitical Context: Conflict and Isolation

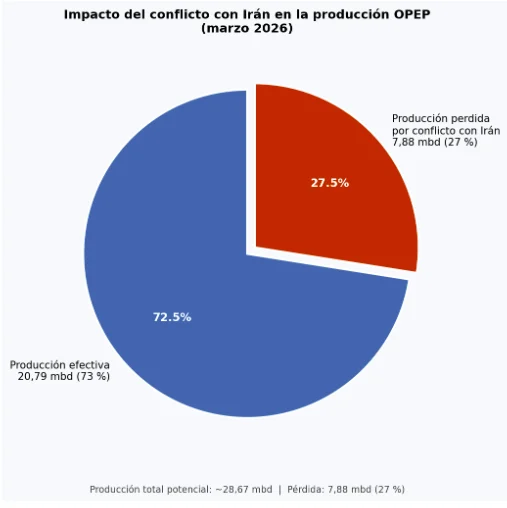

The UAE’s exit does not occur in a vacuum; it is framed within a highly volatile regional environment. The ongoing conflict with Iran has had a devastating impact on OPEC’s productive capacity. In March 2026 alone, the war eliminated 7.88 mbd of production, representing a 27% loss and reducing the cartel’s effective production to 20.79 mbd.

Adding to this scenario of supply scarcity is the military blockade of the Strait of Hormuz, a vital artery through which a fifth of global oil and liquefied natural gas passes. Although the UAE has a pipeline to the port of Fujairah in the Gulf of Oman, it is already operating at maximum capacity, limiting export alternatives.

Furthermore, the break formalizes a deep geopolitical rift with Saudi Arabia. Tensions over regional leadership, exacerbated by divergences in conflicts such as Yemen (where Saudi airstrikes affected Emirati allies in December 2025) and the management of the Iranian crisis, have destroyed the traditional solidarity of the Persian Gulf.

Long-Term Perspectives and Consequences

The UAE’s exit leaves Saudi Arabia in a position of isolation, assuming alone the burden of stabilizing the oil market. Although in the short term crude oil prices will likely remain elevated due to the geopolitical risk premium and disruptions in the Gulf, the medium and long-term outlook points towards greater volatility.

Once the conflict is resolved and transit through Hormuz is restored, the injection of unrestricted Emirati crude will flood the market. This anticipates a scenario of greater supply, cheaper energy, and the latent risk of a price war.

Likewise, there is a strategic risk of a “domino effect.” Countries like Iraq or Kazakhstan could observe the Emirati precedent and consider leaving OPEC as a legitimate way to maximize their own production and revenues.

In conclusion, the UAE’s exit not only structurally weakens OPEC, reducing its market share to historic lows, but also signals the possible end of the era in which the cartel dictated the designs of the global energy market. We are entering a period of reconfiguration of alliances, where flexibility and national production capacity will take precedence over restrictive multilateral agreements.

If you found it interesting, please share it!

Recent Articles